Yahoo Sport

Yahoo Sport

Bitcoin Is Macro, but Not ‘Correlated’ in the Way You Think

“Bitcoin is correlated!”

I often hear that thrown out in conversations as a dismissive way of saying that it isn’t really an “alternative” asset at all, and that all this mumbo jumbo about it being external to the broader economy is just "hopium." But very few who say this have actually dug into the data or thought about the reasoning behind that claim (which is understandable – why mess with convenient narratives?). I confess that even I used to think that the surge in the correlation between bitcoin (BTC) and the S&P 500 was because the institutional investors marched into the market in the second half of last year. Now I’m not so sure. The institutions did indeed march in, and bitcoin has to a large extent become a macro asset. But I don’t think that’s driving the correlation data.

Noelle Acheson is the former head of research at CoinDesk and sister company Genesis Trading. This article is excerpted from her Crypto Is Macro Now newsletter, which focuses on the overlap between the shifting crypto and macro landscapes. These opinions are hers, and nothing she writes should be taken as investment advice.

Before we start looking at charts that tell a different story, let’s have a think about what correlation actually means, and why we care. In theory, correlation is simply the measure of the degree to which the movements of two series are related. It measures how much two measures vary together, divided by how much they usually vary individually. (There are other types of correlation with different formulas, but that’s too nerdy to get into here – for those who care, I use Pearson on a rolling 60-day window.)

Imagine two assets that are clones of each other. How much they move independently will be exactly the same as how much they move together, so the ratio between the two factors will be 1. A correlation of -1 means they move perfectly in the opposite direction. A correlation of 0 means there is no obvious relationship between the two.

In reality, these “perfect” situations never exist. Correlations are generally a messy amalgam of erratic behavior that indicates strong or weak relationships, used by investors to design relatively robust portfolio strategies and by analysts and storytellers to spot changes in trends.

Yet, one trap many fall into is to treat correlation as a binary condition. To say something “is” correlated is vague and inaccurate. Highly correlated, negatively correlated – those qualifications make sense, yet even then only at a specific point in time. As we will see, when it comes to market relationships, especially concerning an asset as young as bitcoin, things change fast.

Another frequent trap is to assume that a high or low correlation can explain behavior. To some extent this is true – but more often than not, the relationship is coincidental even if related. Ice cream sales and cases of sunburn are highly correlated, but one does not cause or explain the other.

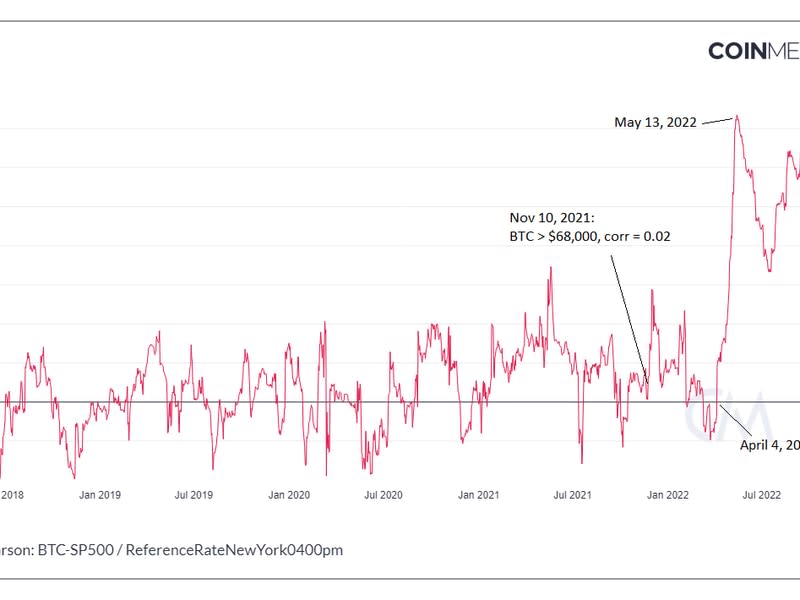

Back to bitcoin. As you can see below, the asset used to be pretty much uncorrelated to the S&P 500 (oscillating around 0) even as the institutions marched in, pushing the BTC price to an all-time high in November. But something changed in April 2022.

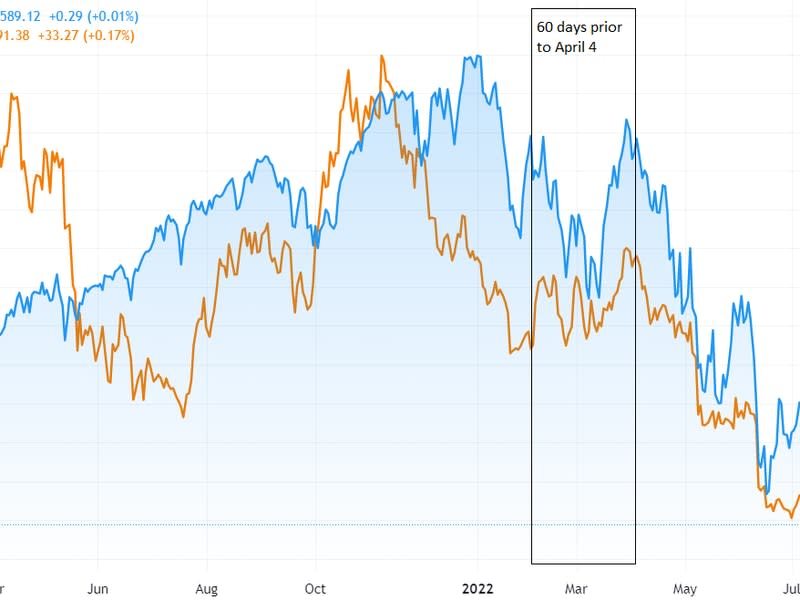

What changed? The overall market mood. Correlation is more about the direction than the size of the price moves (although both matter). The below chart shows that, up until the time that the 60-day BTC-S&P 500 correlation had crossed 0 on the way up (never to return?), the two series had sort of been moving in sync but not really. By April 4, the S&P 500 was down 0.7% on the year while BTC was down 7.5%, and the 60 days prior (the snapshot window for the correlation calculation on any given day) showed different trends for each.

What triggered the mood change? Interest rate expectations. Fed funds above 2.50% started to become a remote possibility in terms of market pricing in early April 2022 (when the actual range was 0.25%-0.50%).

This freaked the market out, and the macro investors who piled into the crypto market over the previous nine to 10 months exited in a hurry. They didn’t just exit crypto (a high-risk asset relatively easy to sell), they also exited equities. Prices fell across the board, and the 60-day correlation between bitcoin and the leading stock index rocketed up to an all-time high of 0.72. Macro investors weren’t the only ones de-risking – crypto fund managers were also exiting, expecting a general market slump.

The spike in correlation was not because bitcoin was now a “macro asset” – bitcoin’s entrance to general portfolios had been more or less consolidated the previous year. It was because bitcoin, along with other “risky” assets, was being hit by expectations of monetary tightening. Semantics, perhaps – but it matters, for the same reason that sunblock manufacturers are in a very different business than ice cream makers even though their sales can move together at certain times of the year.

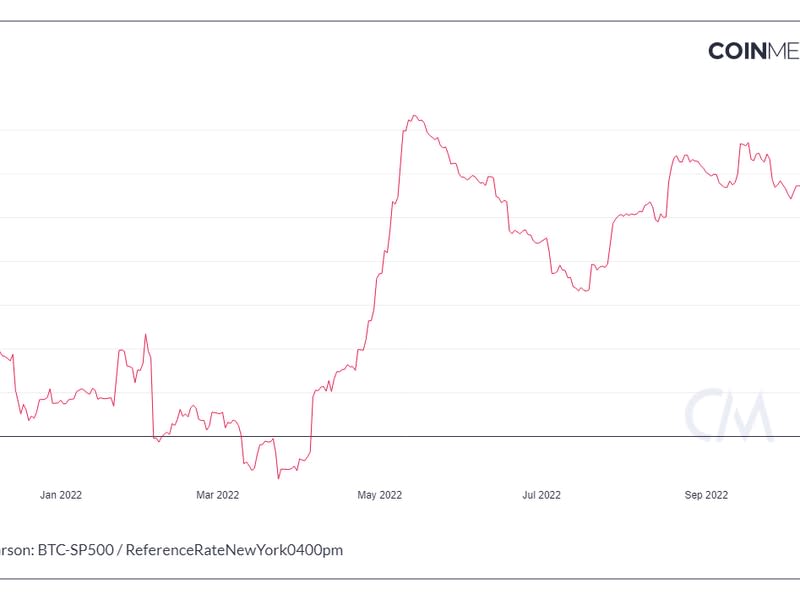

Then, in mid-May, came the implosion of the Terra stablecoin ecosystem. This was a crypto-specific crisis and, unsurprisingly, correlations fell as the damage to crypto values far exceeded that in equities. The de-leveraging triggered by the collapse of hedge fund Three Arrows Capital led to a further decoupling.

With that digested, correlations are on their way up again. But this is not, contrary to common perception, necessarily because bitcoin and stocks are joined at the hip. There’s an old adage that says that “in times of fear, all correlations go to 1.” We are in times of fear. But bitcoin and stocks have very, very different value premises, so we cannot assume the correlations will remain high.

Bitcoin is a macro asset in that it is now part of the global market. But not all macro assets are highly correlated. As fear subsides (which it will, one day), given the distinct value propositions of equities and crypto, we are likely to see correlations head back to lower levels, supporting the narrative of an “alternative” macro asset. Even before then, as the dust settles on the recent crypto crashes, as the outlook for global equities continues to get worse and as the risk of holding dollars shifts higher, we could see investors calibrate the relative downsides of asset groups. The resulting flows of funds are likely to change correlations and narratives, driving a new momentum that impacts correlations even further.

So, it is correct to say “bitcoin is macro,” now and going forward. To say “bitcoin is correlated,” however, requires more nuance and explanation, especially to emphasize that the numerical relationship may be convenient for the moment, but it does not mean what many think it does. And it is almost certain to change.